Personal Background Can you tell us a little about your background before starting your company?

After spending the majority of my career in big corporate, I took a step into entrepreneurship almost 8 years ago. I have never looked back! The truth is that my time in corporate – solving big problems across different businesses across many geographies -these experiences certainly prepared me for addressing the challenges of starting and scaling a new business

Company Journey How did you start your company? What were the first steps you took to get it off the ground and how did you identify the need for your product/service in the market?

HighPeak was formed before I joined just under 2 years ago. I took the helm as the first employee – and took on every role from CEO, to CFO to CPO. I leaned into listening to the market signals and meeting customers with a product that addressed one of the biggest unknowns in retirement – the future cost of healthcare and long term care.

Innovation & Impact What innovations or unique features set your company apart from others in the industry?

Prudential is our investor, and with that comes not only a breadth of resources but also access to the proprietary data of the business. That data is one of our biggest differentiators in market. Leveraging these inputs our data scientist have developed some incredible IP and delivered unique personalized insights for use by advisors with their clients.

Growth and Strategy What has been the most effective strategy for scaling your business?

Everything we build is right for us at a certain point of our journey, we don’t try to over engineer any process or system. BUT we do always build with the end in mind which means recognizing that there are building blocks that lay the foundation for the organization we aspire to become.

Advice & Insights Looking ahead, what are your goals for the future of your company?

We aspire to be the solution of choice for healthcare and longterm care cost estimations that advisors use to support their customers as they navigate n their retirement planning journey.

Company Overview Vic Yeh is Co-Founder & CEO at Cara, a domain-specific AI platform purpose-built for insurance—a modular system that enables agencies, brokerages, and MGAs to automate servicing, accelerate sales, and scale operations with a 24/7 digital workforce. Learn more at getcara.ai.

Can you tell us a little about your background before starting your company?

Before starting Cara, I was an early engineer at Blend ($BLND), a fintech platform powering digital banking experiences for institutions like Wells Fargo and US Bank, across mortgages, account opening, and insurance. At Blend, I helped launch multiple product lines and scale the platform to handle billions of dollars in transaction volume.

Alongside that, I was investing in early-stage software and fintech startups at Polymath Capital, where I had the opportunity to witness startups growing from zero to venture scale.

Those experiences gave me a deep appreciation for the complexity of financial services and the opportunity to use technology to transform legacy industries. The lessons ultimately led me to team up with Nikhil and Jon—friends from Stripe and Strategy&—to build Cara.

What inspired you to become a founder, and how did you identify the need for Cara in the market? I’ve always believed that when applied thoughtfully, technology can be one of the most powerful forces for improving society. Yet insurance—one of the largest and most critical industries—has historically lagged in adopting modern tools.

At Blend, I had my first glimpse into the outdated, manual workflows that still dominate the insurance space. My co-founders, Nikhil and Jon, brought deep experience from Stripe and Strategy&, and together we saw a unique opportunity to use our backgrounds in financial technology to bring innovation to insurance.

How did you start your company? What were the first steps you took to get it off the ground? We started by building a next-generation insurance brokerage, previously known as Oyster. As we scaled to thousands of policyholders, it became clear that revenue growth in insurance requires overcoming labor-intensive, repetitive workflows—without dramatically increasing headcount.

To address that, we built the world’s first AI Copilot for commercial insurance agents, powered by large language models. Initially deployed within our brokerage, the Copilot quickly proved its value by delivering measurable ROI and streamlining agent workflows. That internal success sparked strong demand from other agencies and brokerages. What began as an internal tool has since grown into something much bigger.

We call it Cara.

What innovations or unique features set your company apart from others in the industry? Cara is a domain-specific AI platform purpose-built for insurance—a modular system that enables agencies, brokerages, and MGAs to automate servicing, accelerate sales, and scale operations with a 24/7 digital workforce.

As the industry’s first Agency Intelligence System, Cara is designed to automate back-office and manual workflows—allowing staff to focus on generating premiums and building client relationships.

What sets Cara apart is its built-in deep insurance knowledge and customizability. Each insurance firm configures Cara to fit its unique needs—whether that’s automating coverage comparisons, handling inbound calls through Voice AI, or building custom workflow automations. And because Cara learns from every interaction, it becomes more effective over time.

What has been the most effective strategy for scaling your business?

Word of mouth has been our most powerful growth engine. Many of our customers hear about Cara from industry peers—agencies and brokerages that have experienced firsthand how it transforms back-office operations and drives business results.

We believe that for AI to succeed in a high-barrier, heavily regulated industry like insurance, it must be domain-specific and vertically integrated. That’s why we’ve purpose-built Cara to align deeply with how insurance agencies and brokerages actually operate.

We stay close to our customers—constantly learning from their workflows and evolving use cases. As we continue to deliver measurable outcomes, our customers become our strongest advocates for growth.

Vijaykant Nadadur, Co-Founder & CEO of KnowledgeVerse (K-V AI), an enterprise AI platform purpose-built to automate data-centric workflows over unstructured content—documents, reports, forms, and more. They bring together the power of LLMs, intelligent orchestration, and vertical data understanding to automate repetitive data tasks like extraction, entry, comparison, generation, and search. Can you tell us a little about your background before starting your company?

Before founding KnowledgeVerse, I co-founded and led Stride.AI, an enterprise AI company that delivered intelligent automation solutions for global financial institutions across the US, Europe, and India. That journey exposed me to the hard truths of deploying AI in real-world enterprise environments, where scale, security, and ROI matter far more than hype.

I hold a Master’s degree in Computer Science from the University of Kentucky, where I formally studied Artificial Intelligence, well before it became mainstream. That early exposure to AI fundamentals, combined with over a decade of practical experience in product building, enterprise sales, and customer success, shaped my conviction: the real challenge isn’t AI capability, it’s making AI usable, trustworthy, and impactful inside enterprises.

This belief led directly to the founding of KnowledgeVerse, along with my co-founder Sendhil.

How did you start your company? What were the first steps you took to get it off the ground and how did you identify the need for your product/service in the market?

KnowledgeVerse was born from lessons learned at Stride.AI. After years of implementing AI in highly regulated industries, it became clear that enterprises struggle not with AI theory, but with AI deployment. They needed something better than an LLM playground, they needed a structured, scalable AI platform that could work across fragmented documents, siloed systems, and real-world constraints.

The first step was building our Enterprise AI Stack; a layered architecture with modular “knowledge assistants” that could handle tasks like data entry, extraction, and comparison at scale. We started by working with design partners in pharma and BFSI who had urgent document-centric workflows. These early engagements validated the need and helped us build for scale, not just experimentation.

What innovations or unique features set your company apart from others in the industry?

What makes KnowledgeVerse unique is our purpose-built Enterprise AI Stack for unstructured data. Unlike vertical AI tools, we offer:

5 specialized AI agents for document-heavy workflows: Data Entry, Extraction, Comparison, Generation, and Search

A preprocessing and optimization layer with innovations like semantic chunking, scoped ranking, memory hierarchy, and self-knowledge feedback loops

Plug-and-play workflow orchestration, allowing teams to visually build and automate document processes without code

Enterprise-ready infrastructure with hybrid/self-hosting support, a must-have for regulated industries

We’re not just helping clients “experiment” with AI but we help them operationalize it for regulatory compliance, knowledge management, and reporting workflows that directly impact business outcomes.

What has been the most effective strategy for scaling your business?

Our growth has been driven by a clear strategy: solve high-friction, high-impact enterprise workflows. Instead of being another AI platform vendor, we let enterprises orchestrate their specific workflows to automate painful processes like audit reporting, CAPA document generation, or policy search, to name a few.

Having already earned trust through our work at Stride.AI, we’ve been able to re-engage with many of those enterprises and scale through strong references and deep use case execution.

Another key strategy: platform modularity. Enterprises can start with a single use case and scale horizontally, activating new agents or workflows as needed. This keeps sales cycles lean and value delivery fast.

Looking ahead, what are your goals for the future of your company?

Our long-term vision is for KnowledgeVerse to become the default orchestration layer for enterprise AI workflows. Just as ERP systems manage structured data processes, we believe AI will do the same for unstructured knowledge. Our goal is to power that future.

For entrepreneurs building in enterprise AI:

Don’t start with the tech. Start with the user’s friction. Then build systems that handle complexity, format chaos, integrations, regulatory needs and ensure you keep the experience simple. That’s how we move from demo to deployment.

Jay Patel is Co-Founder & CTO at AviaryAI, a leading provider of voice AI solutions, specializing in enterprise-grade applications for the financial and insurance sectors.

We empower businesses to automate and enhance customer interactions through advanced voice technology, seamlessly integrating with legacy systems.

Their platform enables efficient debt settlement, streamlined customer service, and improved operational workflows, ultimately driving increased efficiency and customer satisfaction.

Question:

What is the background of AviaryAI?

Answer:

Before AivaryAI, we were a group of co founders that started the Cambio Money App.

The Cambio Money App originally started as a NEO bank and a regular FinTech that were helping under underserved communities get access to banking, especially those that had got kicked out of the credit system through something that was check systems.

Through that process, we were trying to figure out how to get people’s credit to go up as quickly as possible.

We started with paper disputes, emails and whatnot, and then when GPT 3.5 launched, it was around the same time as those, those memes with the Presidents playing Minecraft with each other, and I was like, Wait, we can just take the voices and that whole tech and just put it on the phone and settle people’s debts that way.

And that’s kind of how AviaryAI spawned.

Before AivaryAI, we co-founded the Cambio Money App, a NEO bank for underserved communities. Inspired by GPT 3.5, we shifted to voice technology for debt settlement, leading to AivaryAI’s development

Question:

What are some of the challenges that your team has faced in the earlier stages?

Answer:

So the pivot was really tough because we we were trying to build the version that helped settle people’s debt in tandem with the version that aligned with enterprise, like interests.

They just could not go like work together, because the one that’s trying to settle people’s debt is honestly a little just more aggressive than what was available to the enterprise, because it’s, it’s different, right?

You’re in a negotiation mode versus, you know, trying to be a pleasant consumer facing customer service agent, right? But then, even after that, and we shut down the old company, the biggest thing was educating our users on AI.

You know, most people like when they got to play with chatgpt, most people just put something in there, treated it like Google and left right, and that’s kind of where a lot of our clients sit, and especially the people who end up actually using our software after people procure it.

It’s people that tried champion chatgpt Maybe once or twice, and now we’re giving them this agent that they have to go set up and configure and basically get it to do good work on their behalf.

So currently, our process is still super high touch, even though we have software in place that lets them do it themselves, just everyone’s so scared to do it wrong, especially because you’re making outbound calls to people you know you don’t want to ruin your brand’s reputation and whatnot.

And that’s that’s a big hurdle for them to go over. So what we do now is we have a customer success team that goes and essentially builds their first one or two for them, and then, going forward, we actually built an AI based on the notes from every previous ones of our customers that’s going to walk through and build your first couple use cases for you.

Going forward, maybe that’s going to launch in about three weeks, but yeah, the biggest thing has just been, one, after the sale, getting the actual business users to use it.

And two, once they see value, they can champion it for us to their IT teams to actually start integrating us their internal technology.

Question:

Can you share any memorable or defining moments that have helped shape this company?

Answer:

When we were first building this stuff, we knew that we wanted to do something in the voice AI space, and we had that bot that was originally from the consumer app. So what we did was we went around our network, through our board, and met up with a bunch of people in a bunch of different industries.

So we went and we met up with an overflow call center, we met up with an insurance servicing call center, and we met up with both a credit union and a bank, and we basically spent time figuring out what the best thing to do in this space with our technology was.

So there was a about like a six week period of time where we were building four products simultaneous.

Simultaneously. Um, we built an auditor that basically monitored actual customer service reps scores with like, custom metrics and like a way that people can go and ask, what went wrong on this call?

What’s going wrong on all my calls? In aggregate? We built a real time translation tool.

So let’s say I was speaking in Hindi right now, and you were a customer service rep. On your screen, you would see the English version of what I was saying, and you could type it back in a clone of your own voice.

You would be sounding back to Hindi to me over the phone.

We also built what we’re building today, which is the voice agent, and then the knowledge base. So it was kind of this weird place, especially for me and the engineering team, where we were building four things, and it was like, All right, well, what’s going to get killed here, right? And then, like that, that moment where it was like, actually deciding, like, what products gonna get killed?

Because especially as you’re building, you kind of start falling in love with what you’re building a little bit. So when we finally made that decision and cut down our translator and our auditor services, it was, it was like, Oh, this is real.

And these the knowledge based product and the voice agent are, like, getting traction, and we just need to focus on that. And it just, it finally felt like things were clicking.

Question:

What is the differentiator between AviaryAI and your competitors?

Answer:

There’s definitely a bunch of people in the voice AI space now, the first, but I think we were probably the first verticalized one.

And it’s really that vertical, especially insurance companies and credit unions and some banks, they are running on this really, really old software that’s really hard to integrate into and not really obvious to integrate into.

So there’s like, platforms where you can basically go and build a voice agent for yourself really easily, and, like, hook it up to a tool like everyone knows, like Calendly, but there’s no platform where you can hook up a tool to the back end banking systems of a credit union, and that’s kind of what makes us different.

We’re going to be plug and play for financial institutions and insurance companies from essentially the moment they start their IT. Teams actually begin working with us, like they work with us.

To rephrase that, they do work with us today, but like from sale to when their IT team gets our project, we have that weird in between period where we’re trying to teach the business users how to use the software in the basic state, and then we go to more advanced states.

Question:

What kind of feedback have you received from your customers, and how does that shape your business strategy?

Answer:

So definitely the initial gut reaction for when they try to do something, the first time, they’re just like, Oh, it can’t do all this.

Can it? And then we have to walk them through being like, No, it really can do all of this. And then when they do see it, and they finally deploy their first agent with us, and they start getting their reports back, they’re like, whoa.

This is actually just working. And there’s one of two feedbacks. Awesome.

So, how do I get more data visibility? And then two is, sometimes they go remote, remote, silent. And we always thought that was a bad thing, but they would just come back and be like, what you guys did worked well enough where we just had way too much inbound volume on things to kind of handle, handle it.

So we didn’t want to start another use case yet, but we they kept the contract right, so they’re going to start another use case once they’ve kind of figured it out, and then we have that knowledge based product too.

A big thing with that is we built this knowledge base that helps CSRS spend less time on them. The the big feedback for that one is, once people start using it and they realize they can’t basically tell an AI the tribal knowledge that they have, they kind of realize that their documentation is bad, and they go through this overhaul to make it better, and that makes our product work better with theirs too.

So like a lot of those things that you would hope it makes them reflect on, oh, we had a bad process before, and we have to make it better for our tools to work better. So we’re also now building tools to help them make their stuff better.

Question:

What is your growth strategy?

Answer:

So we have two teams, obviously, me being on the technical side of the FEM team, I’m always concerned to make sure our stuff’s up to stuff. But for the most part, we are. We are either better than the majority of our competitors or competitive with the best one, right?

So it’s not that our technology isn’t there. It’s more just about, how do we make it easier for them to use now? And that kind of increases our sales velocity on like, Oh, it’s so easy to use that you don’t need to get your IT department involved, right?

So it’s a little bit hand in hand, but not really, but because our technology has gotten in such a good place over the last nine months, we’ve kind of just been like, Okay, we just need to get more people in the door. And due to the fact they’re enterprise clients, they just move a little slower.

So we just, we’re now working on, okay, even if they sign the contract and they’re in the door, and we have that as realized revenue, we we want them to be happy with the product too. So it’s like, how do we get them, even after that post buy? How do we get them going as quickly as possible? You know?

So it’s kind of go. It goes in the same way. And also just the the two industries that we’ve really targeted, they’re they’re word of mouth industry is more than like, TV advertisement or podcast advertisement industries, right?

So like, as soon as we start really showing value to a couple of them, the word spread, that’s basically what’s been happening almost every single one of our clients from the last four enterprise contracts we’ve landed had been referrals from a previous client

Question:

What are the short term and long term goals for the company?

Answer:

For the short term, we kind of just want to make it as easy as possible for business users to get as far as possible without dragging their IT resources into it.

So we’re really trying to figure out how to hook directly into some of the providers specifically so they can just drop in their API key, rather than having to go through their API and I go through their IT department.

So it’s really just going from contract sign to value faster now, and that’s kind of our short term goal, because the moment we can do that, especially going back to the whole like our customers are going to talk to our next set of customers, kind of feedback loop that we’re going through here.

If we can get the ones that have just signed today to basically get going as soon as possible, it’s going to just increase the speed of that. So that’s what we’re really focusing on the next four months, that the naturalness of our voices.

So we’ve been working on a new voice model internally. That’s pretty, pretty good, but we’re trying to get fast.

Long term, there’s, there’s a couple different plays going on here, given the tools that we it we’ve talked about is we kind of want to make those tools accessible to other AI tools and build like a marketplace, maybe around that as well, so it no one has done what we’re doing because it’s really hard and very annoying to do so, and you kind of need, like the right contacts to do in so if we can make it easier for other developers and other like companies to set up shop, that kind of just opens a whole new can of worms of just now, not only are we going to be The best chat agent for enterprises in this space to use.

We’re going to have the best voice outbound agent, the better enterprise can use. And now, when other people from other spaces or tools that they’re already using can’t hook into their system, we can be that layer that helps those tools hook into their system.

And it just it’s going to be this very cohesive system of just like allowing AIS to work with these older institutions that other development shops focused on.

So it’s finally just kind of giving them the opportunity to modernize all their tools, and hoping that once we do that, and if we can build those adapter layers, that the other providers can come in and start, you know, bring these guys into the present.

Question:

How are you managing your work-life balance

Answer:

it’s gonna sound weird, but it’s gotten a lot better because we have an office now for me, I guess. But like, because we have the office now, when I leave the office, I just try not to do any more work for the most part. But yeah, it’s it’s definitely been difficult.

It’s gotten a little easier, and now that we’re growing, we’re finally hiring more people. So a lot of my time is just it’s spent differently than it used to, like I used to just be hands on keyboard constantly, just basically churning out code these days, just due to, like, the different cycle of work.

Even though I’m probably working more hours than a typical person would, because it’s different kind of work, the burnout doesn’t get to me as much as it used to.

So one that’s super helpful, just being able to kind of transition from different kinds of work and then two, like you gotta, you gotta keep your weekends, right?

You gotta have, like, a day, maybe two days, where you can just make sure you got all your stuff in order, and just at least try not to think about it, so you can come back refreshed. And that’s kind of how I, I handle it,

Question:

What do you do outside of work, to recharge?

Answer:

I longboard when the weather is nice. It’s just nice to put some music on and just go out for an hour or two, and then I’ve been three modeling and 3d printing, just little like, knick knacks.

A lot of my cousins are having kids now, so I just make them toys. It’s fun.

Question:

What’s one fact about you or the company that people might not know?

Answer:

We had a voting session about what the company’s name should be, and I submitted the name, pigeon.ai, and it won, but got vetoed, so we could have been pigeon instead of AviaryAI. So it’s named aviary because, um, we originally started this voice AI company, and going back to the whole pigeon thing, I made my case for it.

Um, I was thinking about messenger pigeons, but then when blessings started presenting it out, he just thought everyone thought it sounded like a like, apparently everyone thinks pigeons are gross. I think they’re kind of cute, but yeah. So he was just like, yeah, no one likes that, but we wanted to keep the bird thing. So it was like,

Okay, well, messenger birds go into an aviary. Or the next answer was pigeon coupe. But you can’t just have the word pigeon in it for some reason.

Yeah. So that’s how we kind of got to aviary, and it’s really funny, all of our internal services inside are named after birds. So like, look at all of our code bases. There’s just different bird names. So our our entire GitHub just looks insane.

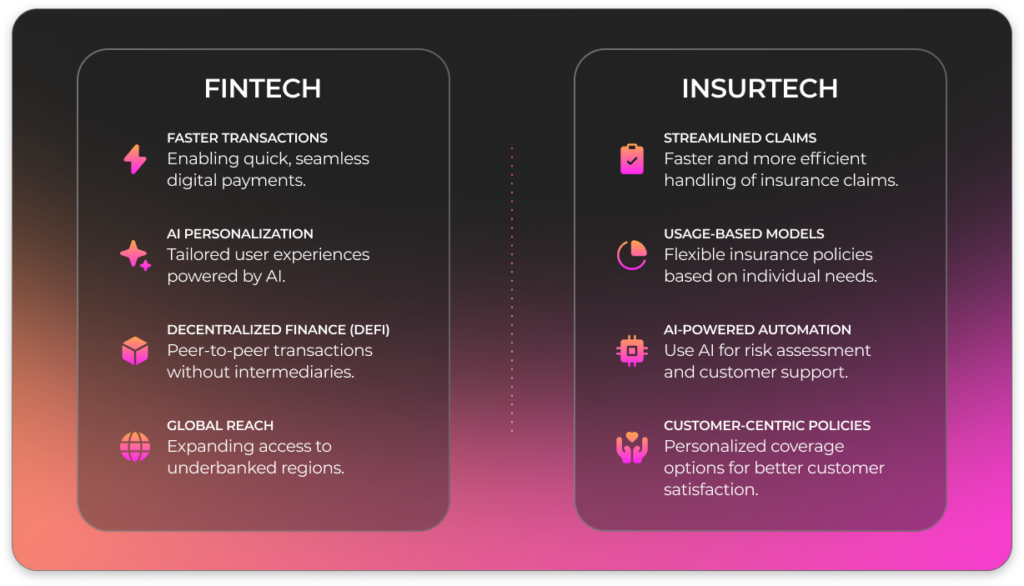

The Blueprint Tour San Francisco delivered high-impact discussions on fintech, insurtech, and healthtech.

With expert panels, a live startup pitch-off, and exclusive networking, the event fostered innovation and strategic expansion. Coverbase won the pitch-off with its AI-powered vendor management platform, while Wuuii showcased its AI-driven wildfire hazard assessment solution. Hosted by T Palmer Agency, a full-service marketing agency specializing in event marketing services, the event provided valuable insights for founders, investors, and industry leaders.

The Blueprint Tour San Francisco stop united the brightest minds in fintech, insurtech, and healthtech. This event fostered connections, sparked conversations, and showcased innovative startups in the industry’s changing landscape. Sponsored by JobsOhio, the event featured insightful panels on strategic growth and funding. It also included an intense pitch-off between fintech and insurtech. Attendees enjoyed thought-provoking discussions and gained actionable insights.

About JobsOhio

We were proud to have JobsOhio as our sponsor for the Blueprint Tour San Francisco. JobsOhio is dedicated to driving economic growth and innovation by supporting businesses and entrepreneurs in key industries, including fintech, insurtech, and healthtech. Their dedication to promoting innovation and investment aligns well with the Blueprint Tour’s mission. This initiative helps startups gain the resources, funding, and connections necessary for successful growth.

Key Highlights from the San Francisco Stop

Opening Panel: The Art of Strategic Expansion

The event began with the Strategic Expansion: The How, When, and Why panel. This session was moderated by Thien-Nga Palmer, the Founder and CEO of T Palmer Agency. Her agency is a full-service marketing firm that focuses on event marketing services. The discussion featured expert insights from:

Ashlyn Lackey (Director, Innovation Strategy, Prudential) on navigating the challenges of scaling in the insurance sector.

Eugenio González (Partner & Head of InsurTech, Plug and Play Ventures) on the role of accelerators in startup expansion.

David Gritz (Co-Founder, Insurtech NY) on the financial services industry’s evolving investment landscape.

The conversation emphasized the importance of market readiness, strategic partnerships, and sustainable growth strategies for startups looking to expand.

Fintech vs. Insurtech Pitch-Off: A High-Stakes Showdown

One of the event’s most awaited moments was the Fintech vs. Insurtech Growth Startups Pitch-Off. Here, early-stage companies showcased their innovations to a panel of respected judges. In just a few minutes, each startup made strong pitches. They received live feedback from investors and industry leaders.

🚀 Winner: Clarence Chio from Coverbase! After a series of impressive presentations, Coverbase emerged as the winner. It demonstrated its potential to transform the fintech and insurtech sectors with its AI-powered vendor management platform. By optimizing workflows and streamlining operations, Coverbase enhances efficiency and scalability for businesses navigating the any ecosystem.

Other participating startups included PartnerSpace, a platform that simplifies embedded and affiliate partnerships. Another notable participant was Wuuii, which is transforming digital insurance solutions through AI-driven personalization.

Masterclass: The Power of a Strong Brand Identity

Branding isn’t just about logos and taglines—it’s about storytelling, trust, and market positioning. Led by Thien-Nga Palmer, this masterclass explored how founders can build a compelling brand that stands out in a competitive landscape. Attendees gained insights into crafting a brand narrative that resonates with customers and investors alike.

Decoding Funding for Startups: VC Perspectives

Securing funding is one of the most pressing challenges for fintech, insurtech, and healthtech founders. In the Decoding Funding for Startups panel, Suzanne Passalacqua (Managing Director, Carrick Capital), Sarah Kim (Partner, Centana Growth Partners), and Tanvi Lal (VC, Intuit Ventures) shared their expertise on what investors look for, how to structure fundraising efforts, and the key financial metrics that drive investment decisions.

Building Resilient Founders & Thriving Businesses

The day wrapped up with a candid discussion on resilience and sustainability in entrepreneurship. Eric Schneider (Founder & CEO, Akko), Jason Andrew (COO/CIO & Co-Founder, Zoe Foundry), and Hannah Wu (Co-founder & CEO, Amplify Life Insurance) shared their experiences in navigating the ups and downs of startup life, emphasizing the importance of mental well-being, adaptability, and long-term vision.

A Night of Networking and New Opportunities

Attendees mingle and enjoy a cocktail at the Blueprint Tour SF

Attendees network and cheers at the Founders’ Dinner

Networking with the best founders

Creating Connections and Growing Community

Say cheese! Everyone smiles at the 12th Founders Dinner

Following an action-packed day at Stem Kitchen & Garden, attendees gathered for an exclusive cocktail reception. Conversations flowed over drinks, while live music created a vibrant atmosphere. The Founders Dinner later in the evening offered a cozy atmosphere for meaningful conversations. It helped build valuable connections among founders, investors, and industry leaders.

What’s Next?

As the Blueprint Tour progresses through key hubs in fintech, insurtech, and healthtech, we can feel the energy from San Francisco. This excitement sets the stage for our upcoming stops. Whether you’re a founder looking for funding, an investor scouting the next big thing, or an industry leader eager to share insights, the Blueprint Tour is the place to be.

📍 Looking to host an unforgettable industry event? Our team specializes in crafting high-impact experiences that drive meaningful connections. From marketing services to full-service event marketing strategies, we help businesses create experiences that leave a lasting impact. Learn more about our event services today!

The fintech world came alive at Fintech Meetup 2025, an event that delivered high-impact fintech networking, groundbreaking insights, and a showcase of the latest financial technology conference innovations. With

The fintech industry is seeing important trends that are influencing conversations, lively panels, and many meetings. This year’s event fostered a vibrant atmosphere for new business opportunities. It also set a clear direction for the industry’s future.

As a specialized agency in fintech event marketing, branding, and strategic communications, T Palmer Agency recognizes the power of effective fintech events. These events can significantly drive business growth and create a lasting impact in the industry. Here’s a recap of the key highlights from the three action-packed days—and how we can help your brand make waves in b2b fintech marketing.

Day 1: A High-Energy Start to Fintech Meetup 2025

The excitement was palpable as thousands of fintech professionals arrived for the first day of Fintech Meetup 2025. The energy and enthusiasm set the tone for an unforgettable event filled with fintech partnerships, networking, and innovation.

Registration opened bright and early, welcoming attendees from across the fintech ecosystem.

Innovate 360 by J.P. Morgan Payments led engaging discussions on the future of payments innovation, exploring emerging trends and transformative technologies.

Keynote speakers included Michael Rhodes from Ally Financial, Nigel Morris from QED Investors, and Ryan Breslow from Bolt. They discussed important challenges and opportunities in digital banking strategies.

The evening concluded on a positive note with the Welcome Reception, sponsored by Tyfone. This event brought attendees together for a night of connection and fun, investor networking and meaningful connections.

At T Palmer Agency, we specialize in creating strategic event marketing strategies that elevate brand visibility at industry-leading fintech conferences. We also focus on SEO for your fintech blog content. From pre-event social media marketing for fintech to on-site activations, we focus on making your presence memorable. We ensure that your brand leaves a lasting impact on attendees.

Day 2: A Deep Dive into Fintech’s Future

The second day of Fintech Meetup 2025 enhanced the overall experience. It featured a comprehensive agenda focused on fintech trends. Attendees engaged in discussions and participated in deal-making activities.

The Exhibition Hall opened at 9 AM, showcasing cutting-edge B2B fintech solutions and groundbreaking innovations.

The first session of meetings began in Hall C. It featured thousands of pre-scheduled meetings. This environment fostered strong connections and opened doors to new fintech growth strategies.

Colin Walsh, Founder of Varo, shared strategies on mastering digital banking experiences.

A dynamic panel discussion included leaders from M1, Public, DriveWealth, and Betterment. They examined the new factors influencing institutional investing and wealth management trends.

Meetings Session 2 continued the momentum, giving attendees another opportunity to connect, collaborate, and close deals.

The Expo Hall Happy Hour offered an ideal way to end the day. It brought fintech startups together to celebrate, network, and build on the event’s momentum.

Events like this prove the importance of precision-targeted digital marketing strategies to generate awareness and maximize engagement. At T Palmer Agency, we create engaging content marketing for fintech. We also provide paid media services for fintech brands and lead generation for fintech campaigns. Our goal is to help your brand connect with the right fintech professionals before, during, and after the event.

Day 3: A Historic Finish to Fintech Meetup 2025

The last full day of Fintech Meetup 2025 was filled with energy. Attendees engaged in impactful meetings and transformative discussions. The day concluded with an exciting startup pitch competition.

The Exhibition Hall opened again, giving attendees another chance to explore the best and fastest growing fintech startups.

The Startup Pitch Finale named Utsav Shah from Kaaj and Edwin Handschuh from 1Konto as the winners. They triumphed in the much-anticipated fintech startup pitch competition.

A compelling keynote addressed the topic of expanding embedded financial services. It featured insights from Nate Starrett, who is associated with Stripe, and Tom Bianco from Fifth Third Bank. The session was moderated by Sanjib Kalita, Chairman of Fintech Meetup.

Shivani Siroya, CEO of Tala, concluded the keynotes with an inspiring talk. She discussed how emerging technologies are opening financial access and driving global growth.

The day concluded elegantly with the Expo Hall Happy Hour. Attendees shared final insights and strengthened new relationships in the fintech industry.

At T Palmer Agency, we know that great content fuels engagement. We assist fintech brands in enhancing their message. We do this through SEO-optimized blogs, social media recaps, and PR strategies. Our goal is to ensure their thought leadership stands out in discussions after events.

The Grand Finale: HumanX Closing Party

As Fintech Meetup 2025 approached its end, the excitement grew. Attendees eagerly anticipated the HumanX Closing Party at Zouk Nightclub. Attendees gathered for one last chance to celebrate, reflect on the event, and build lasting fintech partnerships.

For brands aiming to enhance post-event engagement, we provide strategic email marketing for fintech. We also offer social media amplification and lead nurturing solutions. These services help maintain momentum long after the event concludes.

Final Thoughts

Fintech Meetup 2025 was an incredible showcase of fintech innovation, fintech networking, and industry leadership. This event featured influential fintech keynote speakers and numerous discussions on institutional investing and digital banking. It reaffirmed its status as a must-attend gathering for fintech professionals.

At T Palmer Agency, we focus on event marketing, digital strategy, and brand positioning. We help fintech companies create a strong impact. If your brand wants to stand out at major financial technology conferences, let’s connect. Together, we can create a fintech marketing strategy that delivers results.

If you missed this year’s event, make sure to mark your calendar for Fintech Meetup 2026 – because the future of fintech events is just beginning its journey!

Interested in elevating your brand’s presence at fintech events? Contact T Palmer Agency today to strategize your next big move!

The Blueprint Tour: NYC brought together fintech and insurtech leaders…

for a day of expert panels, a high-energy pitch-off, and invaluable networking opportunities. From scaling strategies to funding insights, discover the key takeaways that are shaping the future of finance and insurance.

The Blueprint Tour: New York City united leaders from fintech and insurtech, along with investors and entrepreneurs. This event offered a dynamic day filled with insights, innovation, and networking opportunities. On February 13, 2025, the Classic Car Club in Manhattan hosted our event. Attendees enjoyed thought-provoking panels and a high-energy pitch-off. Valuable conversations took place, aiming to shape the future of finance and insurance.

Key Takeaways from The Blueprint Tour: NYC

The strategic expansion panel at Blueprint Tour NYC

Cristina Ciaravalli moderates the strategic expansion panel

Networking with the best cars and founders

From thought-provoking panels to an exciting pitch-off competition, the Blueprint Tour: New York City provided a deep dive into the challenges and opportunities shaping the fintech and insurtech industries. Attendees walked away with actionable insights on scaling businesses, securing funding, and fostering resilience in leadership. Below are the key highlights from each session.

Key indicators signaling when a startup is ready to expand, including revenue stability, customer demand, and operational capacity.

Assessing market readiness versus operational readiness to ensure a successful expansion strategy.

Evaluating new markets and customer segments through competitive analysis and localized testing.

Aligning expansion goals with the overall business strategy to avoid misalignment and unnecessary risks.

Critical operational elements such as team structure, infrastructure, and scalable processes that must be in place before scaling.

Common Challenges:

Common challenges startups face during expansion, including resource constraints, misaligned growth strategies, and regulatory hurdles.

Balancing aggressive growth ambitions with sustainable operational practices to prevent financial strain.

Overcoming hesitation around expansion due to concerns about losing control or compromising quality.

A key takeaway: successful expansion requires careful planning, strong leadership, and adaptable execution.

Fintech vs. Insurtech Growth Startups Pitch-Off

The high-energy pitch-off was one of the most anticipated segments of the day. Startups in fintech and insurtech battled it out, showcasing their innovative solutions to a panel of expert judges, including David Gritz(Co-founder, Managing Director, InsurTech NY) and Abdul Abdirahman (Principal, F Prime Capital).

Growth Startups Pitch Off

Eric Chu from Tradedesk

Jean Smart from Penelope pitches to win

The founders celebrate after their successful pitches at Blueprint Tour NYC

Startups that took the stage:

Aviary AI– Jay Patel, Co-founder and CTO – A Voice AI-powered engagement tool for financial institutions, automating customer outreach and reducing human operator time. The company has seen a 42% pick-up rate and 71% interaction rate, proving its efficiency in customer communications.

Tradesk Securities – Eric Chu, CEO – A fintech-powered broker-dealer providing AI-driven investment research tools for retail investors. With 23,000+ customers and 31 software patents, Tradesk is revolutionizing digital trading with real-time insights and zero-commission investing.

Penelope – Jean Smart, Founder and CEO – A next-generation retirement savings platform designed for micro and small businesses, simplifying 401(k) plans with an intuitive, affordable, and automated approach. Penelope serves a diverse client base, with 42% minority-owned businesses and 61% women-owned businesses.

Pitch-Off Winner:

Jay Patel won the Pitch-Off with Aviary AI, showcasing the power of Voice AI in transforming customer engagement for financial institutions.

Cristina Ciaravalli from Valli Ventures moderates this panel

The panelists prepare for Decoding Funding

Anna Garcia from Altari Ventures

The discussion heats up between the panelists

Jay Novis from QBE Ventures

Adam Chadroff from Equal Ventures

Key Topics Discussed:

Fundraising in Today’s Environment:

The funding landscape for early-stage startups in 2025 remains competitive, with investors prioritizing sustainable growth over rapid scaling.

Founders have multiple options to fundraise, including venture capital, angel investors, crowdfunding, and revenue-based financing.

Balancing the need for funding with ownership retention remains a key challenge for founders, requiring careful negotiation and financial planning.

Avoiding overfunding or underfunding is critical to ensure startups grow sustainably without unnecessary dilution or financial strain.

Path to Fundraising for Founders:

Determining the right time to fundraise is dependent on achieving key milestones, such as product-market fit, revenue traction, or customer adoption.

Investors look for specific metrics at different funding stages, from early traction and ARR growth to customer acquisition cost and lifetime value.

Personal and professional networks play a significant role in securing funding, often leading to warm introductions to investors.

Success stories from startups that navigated the funding process effectively emphasized the importance of persistence, strategic networking, and having a clear value proposition.

Tips & Tricks:

Common mistakes startups make include pursuing funding too early without a validated product or waiting too long and missing market opportunities.

Founders should develop a compelling pitch that highlights market opportunity, traction, and financial viability.

Before engaging with investors, startups should refine their financial models and prepare to answer tough questions about growth, burn rate, and scalability.

Building Resilient Founders, Thriving Businesses

The panel on Building Resilient Founders is about to begin

T Palmer moderates the panel

Sharon Rodriguez from Highpeak lights up the stage

Sharon makes the point that resiliency is key to succeed

Resilience for founders means adapting to constant challenges while maintaining a long-term vision.

Balancing work-life responsibilities is essential to prevent burnout and maintain productivity.

Prioritizing physical health—through exercise, mindfulness, and rest—is crucial for sustained energy and decision-making.

Ensuring business sustainability requires thoughtful financial planning, strong team culture, and adaptability.

Cultivating a Healthy Work Culture:

Company culture plays a critical role in fostering resilience across the entire team, not just the founder.

Implementing policies that promote physical and mental well-being positively impacts company performance and employee satisfaction.

High-performance cultures should balance ambition with well-being to prevent burnout among employees.

Leadership must set the tone for a workplace culture that prioritizes health, wellness, and overall team support.

The Power of Networking at The Blueprint Tour: NYC

Setting the stage for networking at the Blueprint NYC

Attendees mingle during the cocktail hour

Guests pose for photos while networking

The power of networking is enhanced with the vibrant atmosphere

Networking with the best cars and founders

Networking can be the source of new business

Attendees pose for photos

T Palmer and her team

Making connections at Blueprint NYC

Ariel and her team

The most unlikely of connections at Blueprint NYC

The perfect prop for a photo

Behind the scenes at NYC

Jay from JET networks at Blueprint NYC

Saying Goodbye to NYC

Beyond the panels and pitch-offs, the Blueprint Tour emphasized networking as a key driver of success. The cocktail reception and Founders Dinner provided attendees with exclusive opportunities to connect with investors, industry leaders, and fellow entrepreneurs.

Looking Ahead: The Next Stop on The Blueprint Tour

📍 Next Stop: NASCAR Hall of Fame, Charlotte, NC on February 25th, 2025– Find more details here!

💡 Want to be part of the next Blueprint Tour event? Secure your spot today and connect with industry pioneers shaping the future of fintech and insurtech.

This article highlights the critical reasons fintech and insurtech startups fail, backed by failure statistics and real-world examples.

It also offers strategies to overcome challenges in funding, market fit, and regulatory compliance. Keywords: fintech failures, insurtech challenges, startup survival, fintech insights.

The world of fintech and insurtech startups is a thrilling ride. It’s a landscape filled with innovation, disruption, and potential for significant financial rewards.

However, it does involve certain risks.

The stark reality is that many of these startups fail. Understanding why they fail and the statistics behind these failures is crucial. It can provide valuable insights for founders, industry analysts, and journalists alike.

This article delves into the top 15 must-know fintech and insurtech startup failure statistics. It’s a comprehensive exploration of the challenges these startups face. It’s also a guide to navigating the complex terrain of financial and insurance technology.

We’ll look at the overall failure rates of startups. Start to examine the unique hurdles that fintech and insurtech startups must overcome. Finally, we’ll explore the reasons behind these failures, from lack of market fit to regulatory challenges.

We’ll also delve into the critical first year of operation. This period often determines whether a startup will survive or join the ranks of failed ventures.

Geographic and sector influences will also be discussed. We’ll consider how these factors can impact a startup’s success or failure.

The role of funding, particularly in the early stages, will be another key focus. We’ll look at how it can make or break a startup’s survival chances.

Finally, we’ll explore strategies for success. We’ll highlight the importance of innovation, customer experience, and strategic partnerships.

This article is not just about understanding the statistics. It’s about learning from them. It’s about using this knowledge to make informed decisions and strategies.

This article is for fintech startup founders, insurance industry analysts, and financial technology journalists alike.

It’s a deep dive into the dynamic world of fintech and insurtech startups.

Let’s begin by exploring the top 15 must-know fintech and insurtech startup failure statistics.

Understanding the Fintech and Insurtech Landscape

The fintech and insurtech sectors are rapidly evolving, driven by technological advancements and changing consumer behaviors. These industries are known for introducing innovative solutions that redefine financial and insurance services.

Fintech startups focus on enhancing financial transactions and services. They integrate technology into traditional finance, offering products that ease money management. Insurtech startups, in contrast, aim to revolutionize the insurance industry through technology.

The fintech industry is vast, covering areas like payments, lending, wealth management, and blockchain. Each sub-sector presents its own opportunities and challenges. Insurtechs often aim to streamline processes, improve customer experiences, and reduce costs within the insurance value chain.

The landscape is competitive and complex, attracting a mix of entrepreneurs, investors, and established firms. Startups must navigate regulatory environments, engage in strategic partnerships, and adopt cutting-edge technologies. Success requires staying ahead of regulatory changes and understanding market needs.

The synergy between fintech and insurtech is fostering a new era in financial services. As these startups push the boundaries of innovation, they also face unique obstacles. Addressing consumer demands and maintaining trust while managing technological and regulatory risks is crucial for these firms. The journey is challenging but offers immense growth potential for those who can effectively adapt and innovate.

The Stark Reality: Startup Failure Rates Across the Board

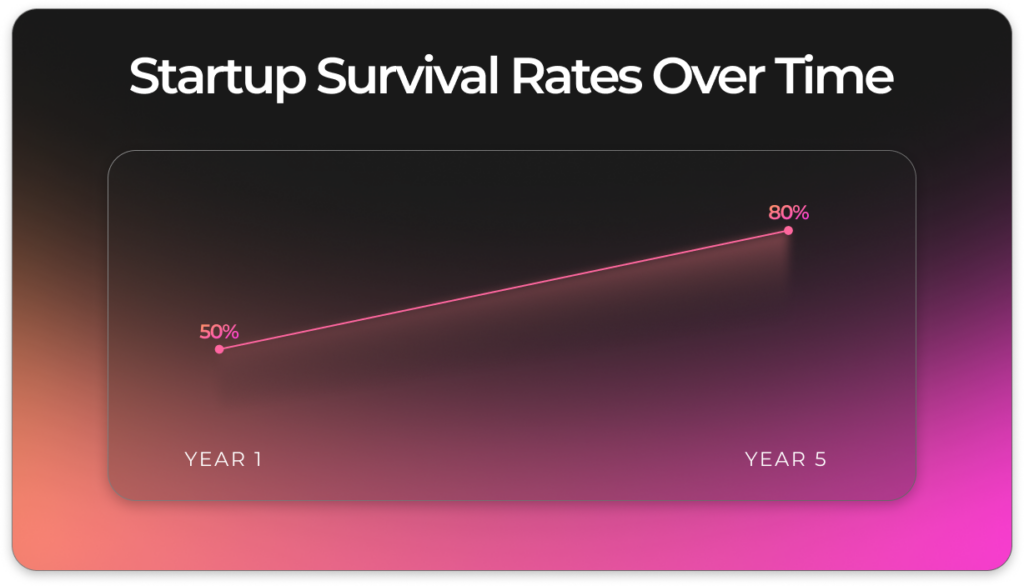

Startup failure is an undeniable reality. Studies show a grim picture: around 90% of startups do not survive. This high failure rate underscores the intense challenges faced by new ventures.

Failure rates vary across sectors. However, they often hover around similar benchmarks. Startups must tackle a range of obstacles, including market competition and financial constraints.

Specifically, around 20% of startups fail within their first year. This period is critical, as businesses strive to establish their presence and attract customers. By the fifth year, about 50% have succumbed to various challenges.

Several factors contribute to these high failure rates. Lack of market demand, poor management, and financial woes are common culprits. Additionally, failure to adapt to changes in consumer preferences can be detrimental.

Other significant issues include high operational costs and insufficient revenue generation. Startups often struggle with balancing expenditures against profits in their early stages. The following reasons are among the most cited:

Lack of a strong value proposition

Poor or ineffective marketing strategies

Inability to scale the business model

Weak team dynamics and leadership

Misjudgment of customer needs or market size

The pressure to innovate and compete in a fast-paced environment is immense. Founders must be prepared for setbacks and be adaptable, as the road to success is rarely linear.

Fintech and Insurtech Specifics

In the fintech space, startups face distinct hurdles. Trust is a major issue, as consumers are cautious about financial services. Building a credible reputation is crucial for fintech startups.

Insurtech startups also encounter unique difficulties. Compliance with strict regulatory frameworks often poses a significant barrier. Navigating such frameworks requires substantial resources and expertise.

Finally, high customer acquisition costs further strain these startups. Competing with established firms for consumer attention and loyalty is an uphill battle. Understanding and addressing these specific challenges are key to navigating the competitive landscape of financial and insurance technology.

Top Reasons Why Fintech and Insurtech Startups Fail

Understanding the reasons behind fintech and insurtech startup failures is crucial. Each startup’s journey is unique, but common threads often emerge. These threads reveal deep-rooted challenges in the industry.

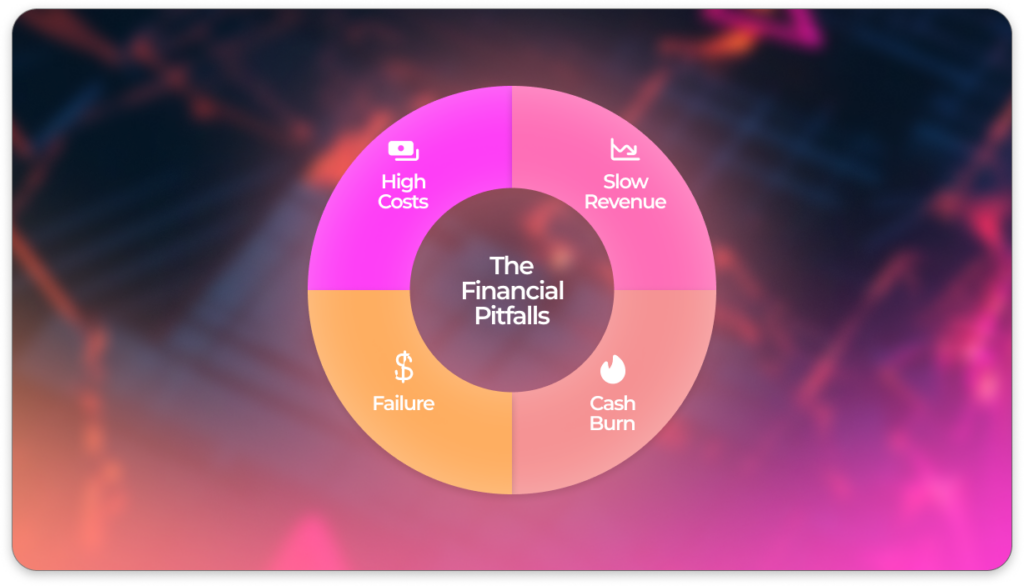

The absence of a strong product-market fit often tops the list. This occurs when startups fail to address genuine consumer needs. The market may be saturated, or the product may not resonate with potential users.

Another significant factor is financial mismanagement. Many startups run out of capital before they can secure sustainable revenue. High cash burn rates and unforeseen expenses can deplete resources rapidly.

Technological barriers also play a critical role in failures. Innovation is essential, but so is integration with existing systems. Many startups underestimate the complexity of this task.

Cybersecurity threats amplify these technological challenges. Breaches can erode trust, leading to a loss of customers and credibility. The sensitive nature of financial data demands robust protection measures.

Regulatory hurdles further complicate the landscape. Navigating complex regulations requires significant expertise and can be time-consuming. Non-compliance can lead to fines or shutdowns.

Operational inefficiencies contribute to downfall too. Poor management and lack of strategic planning can lead to missed opportunities. Founders need to wear many hats, and failing to prioritize can be detrimental.

Ultimately, the success or failure of a startup hinges on its ability to address these challenges. By understanding and preparing for these risks, startups can enhance their chances of survival.

Lack of Market Fit and Customer Acquisition Challenges

A common issue for fintech and insurtech startups is a lack of market fit. This occurs when a product fails to meet consumer needs. Understanding the target market is crucial to avoid this pitfall.

Customer acquisition presents another hurdle. The financial sector is crowded, making it difficult for new players to stand out. High costs of acquisition can drain resources quickly.

Many startups struggle to distinguish themselves from competitors. Without a unique value proposition, attracting loyal customers is challenging. This makes breaking into the market all the more difficult.

Effective marketing strategies can mitigate these challenges. Startups must be agile and responsive to consumer feedback. By doing so, they can refine their offerings and better serve their target audiences.

Capital and Cash Flow: The Financial Pitfalls

Financial mismanagement is a significant threat to startups. Many lack sufficient capital to sustain operations long-term. Cash flow management is critical but often overlooked in early stages.

Startups frequently run out of cash before achieving profitability. This is due to high operational costs and slow revenue growth. The need for ongoing funding is a constant pressure.

Securing investments is vital, yet challenging. Investors are cautious about high-risk ventures. Without adequate funding, startups may struggle to scale or even survive.

Cost control is essential to avoid financial pitfalls. Founders must balance spending against income. By maintaining financial discipline, startups improve their survival prospects.

Technological Hurdles and Cybersecurity Threats

Technology is both an enabler and a barrier for fintech and insurtech startups. Developing cutting-edge solutions is essential but fraught with challenges. Integration with existing systems can be complex and resource-intensive.

Startups often face high technical demands. Innovating requires significant expertise, which can be difficult to secure. Additionally, the rapid pace of technological change necessitates constant adaptation.

Cybersecurity threats pose serious risks to startups. Data breaches can lead to severe consequences, including loss of trust and legal issues. Protecting sensitive information is a top priority.

Implementing robust security measures is crucial for survival. Startups must prioritize cybersecurity from the outset. This involves both technological solutions and fostering a culture of awareness among employees.

Startups often underestimate the complexity of compliance. Regulatory requirements vary across regions and can change frequently. Staying compliant requires constant vigilance and adaptation.

Failure to comply can result in severe penalties or shutdowns. Non-compliance can damage reputation and erode customer trust. This makes regulatory strategy a critical aspect of business planning.

Collaborating with legal experts can help mitigate these risks. Building a solid understanding of the regulatory environment is essential. This enables startups to operate legally and ethically, securing their long-term success.

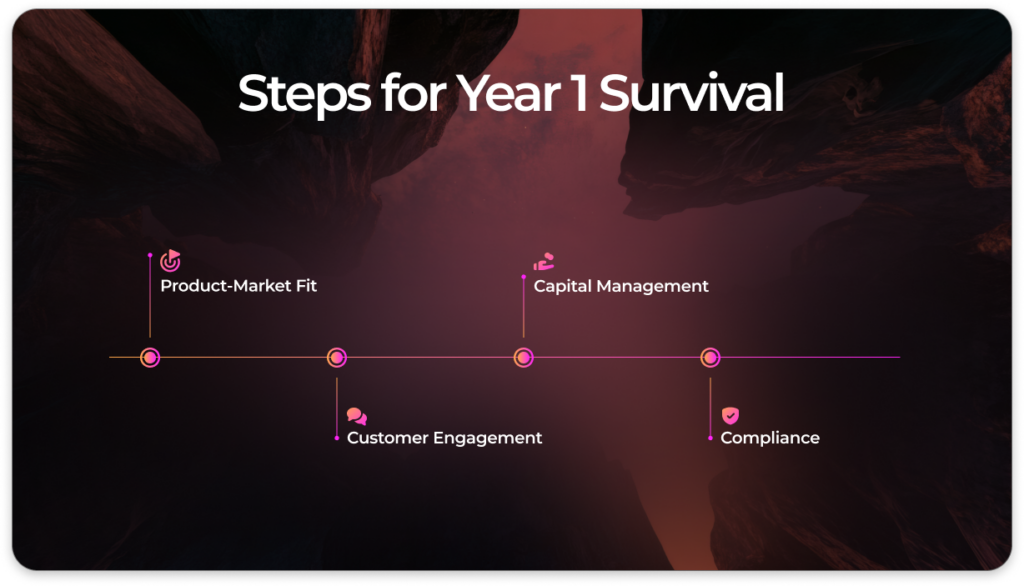

The First Year: A Critical Time for Fintech and Insurtech Startups

The first year for fintech and insurtech startups is pivotal. It’s a period filled with challenges and opportunities that can determine the future trajectory. During this time, founders must keenly focus on building a sustainable model.

Startups face many hurdles early on. Establishing a clear market presence is crucial but not easy. Founders must quickly demonstrate their product’s value.

In this initial phase, agility is an advantage. Startups need to iterate rapidly and adapt to market feedback. Flexibility allows them to pivot as necessary.

Despite the allure of innovation, attention to operational details is vital. Building a competent team and effective processes lays a strong foundation. Ignoring these aspects can lead to early missteps.

Several key elements influence survival during the first year:

Product-Market Fit: Aligning the product with consumer needs.

Capital Management: Efficiently utilizing available funds.

Regulatory Compliance: Adhering to legal requirements.

Technology Development: Ensuring robust and scalable systems.

Customer Engagement: Building and maintaining user relationships.

Each factor interplays with others, underscoring the complexity of startup management in the fintech and insurtech sectors.

The Role of Funding in Early-Stage Survival

Securing funding early is paramount for startup survival. Fintech and insurtech ventures often require substantial capital to achieve their ambitions. This includes developing technology and acquiring customers.

The search for funding is a competitive endeavor. Investors seek viable, scalable models. It’s crucial for founders to articulate a clear vision to attract investment.

Many startups turn to venture capital for growth. However, this comes with pressures for rapid success. Founders must balance growth aspirations against maintaining long-term viability.

Efficient capital management can’t be overstated. Stretching each dollar can buy essential time for iterating and refining the product. This fiscal discipline sets the stage for sustained growth and eventual profitability.

Geographic and Sector Influences on Startup Success

The success of fintech and insurtech startups varies across regions. Geography plays a significant role in shaping opportunities and challenges. Different markets have distinct regulatory environments, consumer behaviors, and levels of tech adoption.

Market maturity influences startup potential. In developed regions, competition is fierce but there’s easier access to advanced infrastructure and capital. Emerging markets, meanwhile, offer untapped potential but demand innovation amid infrastructure gaps.

Sector-specific factors also impact outcomes. Startups focused on payments or lending may face diverse hurdles compared to those in insurance or wealth management. Each sector has its own regulatory and operational complexities.

Understanding local market dynamics is crucial for startups aiming to expand globally. They must navigate cultural differences and adapt business models to new regulatory landscapes. This requires both strategic foresight and operational agility.

Key geographic and sector influences include:

Regulatory Landscape: Varying legal requirements.

Market Saturation: Competition levels in mature vs emerging markets.

Cultural Preferences: Local consumer behaviors and expectations.

Economic Conditions: Impact of regional economic health.

Technological Infrastructure: Availability and accessibility of tech solutions.

Adapting to these factors empowers startups to better position themselves for success in diverse environments.

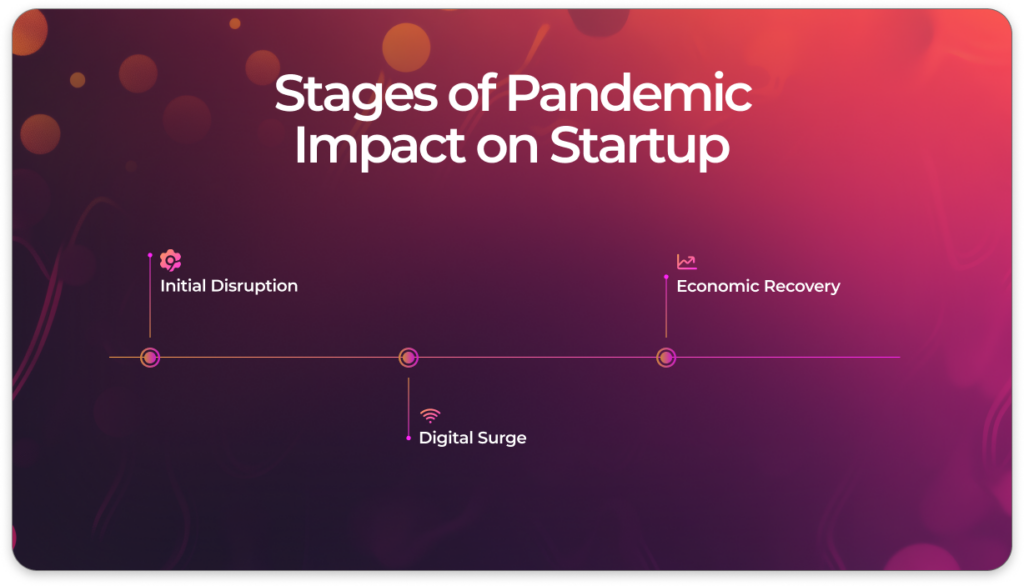

The Impact of the COVID-19 Pandemic

The COVID-19 pandemic reshaped global business landscapes. It accelerated digital adoption, influencing fintech and insurtech startups significantly. Many ventures saw increased demand for online financial services.

Startup resilience was tested. Those with robust digital platforms and remote capabilities thrived. Others had to quickly pivot to survive the new normal, adjusting strategies and operations to meet changing needs.

Despite these challenges, the pandemic presented opportunities for innovation. Startups that capitalized on emerging consumer needs found new growth avenues. This included services like contactless payments and telemedicine-powered insurance solutions.

However, not all weathered the storm equally. Some faced funding cutbacks and operational disruptions. The crisis emphasized the need for agility and preparedness in uncertain times, highlighting the importance of resilience in business strategy.

Strategies for Fintech and Insurtech Startup Success

Navigating the fintech and insurtech industries requires strategic planning. Success hinges on several key approaches that startups must adopt. These strategies ensure not just survival, but the potential for substantial growth and impact.

Firstly, understanding market needs is paramount. A deep dive into customer pain points informs product development. This helps in crafting solutions that resonate with target audiences, increasing the chances of market fit.

Secondly, financial prudence is essential. Efficient cash flow management extends runway, providing crucial time to iterate and refine offerings. Adopting a budget-conscious mindset also supports sustainable operations.

Collaboration is another vital strategy. Partnerships can unlock access to new markets, resources, and expertise. Engaging with established players in the financial ecosystem offers startups a competitive edge.

Key strategies include:

Customer-Centric Approach: Prioritize user feedback.

Efficient Cash Management: Monitor and control expenses.

Strategic Partnerships: Collaborate with industry leaders.

Agile Product Development: Rapid iteration for market needs.

Regulatory Compliance: Stay abreast of changing laws.

By focusing on these strategies, startups can better position themselves to overcome common industry challenges and thrive in a competitive landscape.

Importance of Innovation and Customer Experience

Innovation sits at the heart of fintech and insurtech success. It’s more than introducing new products; it’s about reshaping how financial and insurance services are delivered. Startups must continually push boundaries to stay relevant.

Customer experience is equally crucial. An intuitive and engaging user interface differentiates a brand in a crowded marketplace. Providing seamless experiences builds trust and fosters loyalty among users.

Innovation and customer focus go hand in hand. By leveraging technology to enhance user interactions, startups can create memorable experiences that exceed expectations. This leads to higher satisfaction and retention rates.

Building strong partnerships is a cornerstone for fintech and insurtech growth. Strategic alliances with banks, tech providers, and regulatory bodies offer startups much-needed leverage. These relationships can provide access to wider customer bases and advanced platforms.

Leveraging technology effectively is also vital. Startups should harness the power of AI, blockchain, and data analytics to streamline operations and enhance service offerings. This technological backbone supports scalability and efficiency.

Successful partnerships are mutually beneficial. They allow startups to focus on core competencies while partners fill gaps in expertise or reach. Together, they can tackle complex challenges and unlock new market opportunities.

In the rapidly evolving fintech landscape, collaboration and tech adoption set the stage for enduring success. Startups that capitalize on these strategies gain a robust platform to innovate and expand globally.

Looking Ahead: Trends and Predictions for Fintech and Insurtech Startups

The future of fintech and insurtech holds exciting possibilities. As these industries continue to mature, new trends are beginning to shape their trajectories. Understanding these shifts can help startups position themselves effectively in the evolving landscape.

One significant trend is the rise of embedded finance. Startups are integrating financial services into non-financial products, creating seamless user experiences. This approach is expected to redefine how consumers interact with financial services.

Sustainability is gaining traction within fintech. Consumers and investors are increasingly interested in companies with strong ESG (Environmental, Social, and Governance) practices. Startups focusing on financial wellness and sustainable solutions are likely to attract more attention.

Predictions for the coming years include:

Rise of Embedded Finance: Integrating finance into everyday apps.

Focus on Sustainability: Growing importance of ESG factors.

Increased Personalization: Tailoring services to individual needs.

Expansion of Digital Currencies: Wider acceptance of cryptocurrencies.

Strengthening Cybersecurity Measures: Adapting to emerging threats.

Additionally, personalization is set to take center stage. Consumers prefer services tailored to their unique needs, pushing startups to offer more customized solutions. Leveraging data analytics and AI will be crucial for providing these personalized experiences.

With digital currencies gaining acceptance, startups must adapt to new forms of transactions and investment. This shift presents both challenges and opportunities for innovation.

Lastly, cybersecurity will remain a top priority. As technology advances, so do the threats. Startups need to invest in robust security measures to protect sensitive financial data, ensuring trust and compliance in their offerings.

Navigating the Fintech and Insurtech Ecosystem

Fintech and insurtech startups face a challenging yet rewarding path. Understanding the landscape and embracing innovation are crucial for their survival and growth. The unique hurdles they face, such as regulatory compliance and cybersecurity, require robust strategies and informed decision-making.

By leveraging emerging trends and focusing on customer-centric solutions, startups can carve out their niche in the market. Building strong partnerships, prioritizing user experience, and remaining adaptable to change will be key to navigating the complexities of the fintech and insurtech ecosystem. The journey is not easy, but with the right approach, success is within reach.

FAQs on Fintech and Insurtech Startup Failures

What is the typical failure rate for fintech and insurtech startups?

The failure rate for startups, in general, is high, with fintech and insurtech being no exception. Approximately 90% of startups do not succeed, with a significant number failing to reach their fifth year.

What Leads to the Failure of Fintech Startups?

Fintech startups often struggle with building trust, complying with regulations, and acquiring customers. The competitive market and integration complexities add further challenges.

Are insurtech startups more likely to fail than fintech startups?

Both face significant obstacles, but insurtech startups often contend with stricter regulatory environments. Balancing innovation with compliance is a common hurdle.

How does regulatory compliance impact startup success?

Navigating complex regulatory landscapes can drain resources and time. Startups that fail to comply risk penalties and business closure.

What role do market conditions play in startup failures?

Economic downturns and market saturation can hinder growth. Startups must adapt to these conditions to remain viable.

Is lack of funding a major reason for startup failures?

Yes, insufficient capital is a leading cause. Many startups run out of money before achieving profitability.

How can startups improve their survival chances?

By focusing on customer needs, securing adequate funding, and remaining flexible, startups can increase their likelihood of success.

What technology challenges do fintech startups face?

Fintech startups often deal with complex integrations and rapidly evolving tech trends. Staying updated with technology is vital.

Can partnerships help fintech and insurtech startups succeed?

Yes, strategic partnerships can provide resources, credibility, and access to new markets, enhancing the chances of success.

What advice is there for new fintech and insurtech entrepreneurs?

Be prepared for the hurdles ahead. Focusing on innovation, understanding customer needs, and staying compliant are essential steps.

This article provides actionable insights on resilience and wellness tailored to fintech and insurtech founders.

It covers strategies for managing stress, achieving work-life balance, and building a sustainable startup culture. Keywords: founder resilience, business wellness, fintech strategies, insurtech wellness.

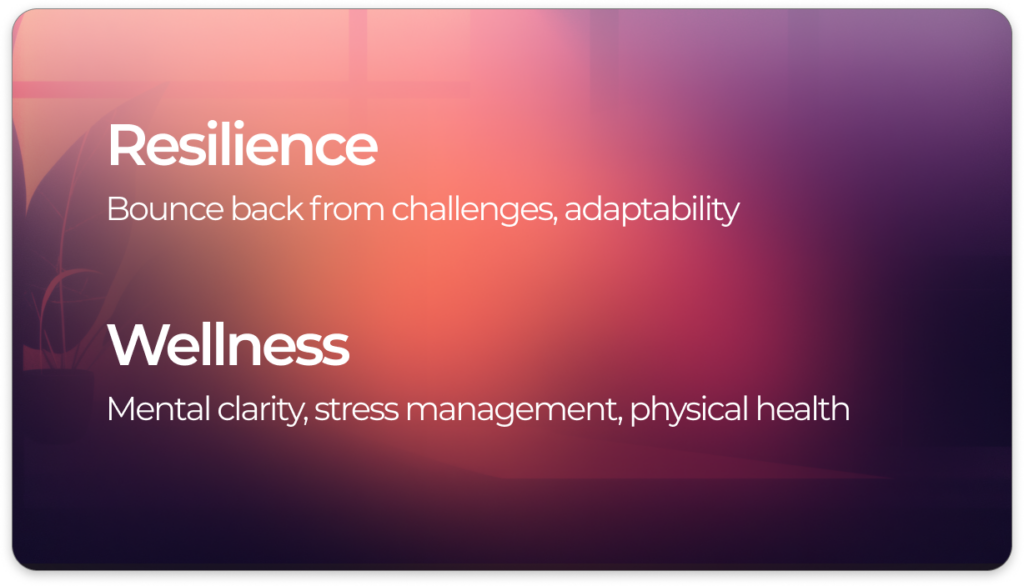

Entrepreneurship is a thrilling journey. It’s filled with opportunities, innovation, and the potential for significant success. However, it also comes with its fair share of challenges. Stress, burnout, and the constant pressure to perform can take a toll on even the most dedicated entrepreneurs. That’s where resilience and wellness come into play. These two elements are crucial for entrepreneurs who want to build stronger businesses and lead more fulfilling lives.

Resilience is the ability to bounce back from adversity. It’s about staying focused and positive, even when things don’t go as planned.

Wellness, on the other hand, is about maintaining a healthy balance in all aspects of life. It involves managing stress, maintaining physical health, and ensuring mental well-being.

In this article, we’ll explore the importance of resilience and wellness for entrepreneurs. We’ll provide practical strategies for stress management and work-life balance, and show how these elements contribute to stronger business foundations and personal success.

Understanding Resilience and Wellness in Entrepreneurship

Resilience and wellness are fundamental components of successful entrepreneurship. Resilience refers to an entrepreneur’s capacity to adapt and recover from setbacks. This quality is essential in the unpredictable world of business.

Wellness focuses on maintaining health in various life aspects. It’s vital for sustained business growth. Entrepreneurs who prioritize wellness are often better decision-makers. Their mental clarity supports innovative solutions to complex problems.

Statistics highlight the prevalence of burnout among entrepreneurs. Chronic stress impacts both personal lives and business outcomes. Understanding these challenges emphasizes the need for resilience and wellness strategies.

Both resilience and wellness intertwine, creating a foundation for long-term success. A resilient entrepreneur, supported by wellness, can face challenges head-on. They are equipped not just to survive but to thrive.

Integrating these concepts into an entrepreneurial lifestyle fosters a balanced, proactive approach to business challenges. It also enhances personal well-being, leading to more sustainable success.

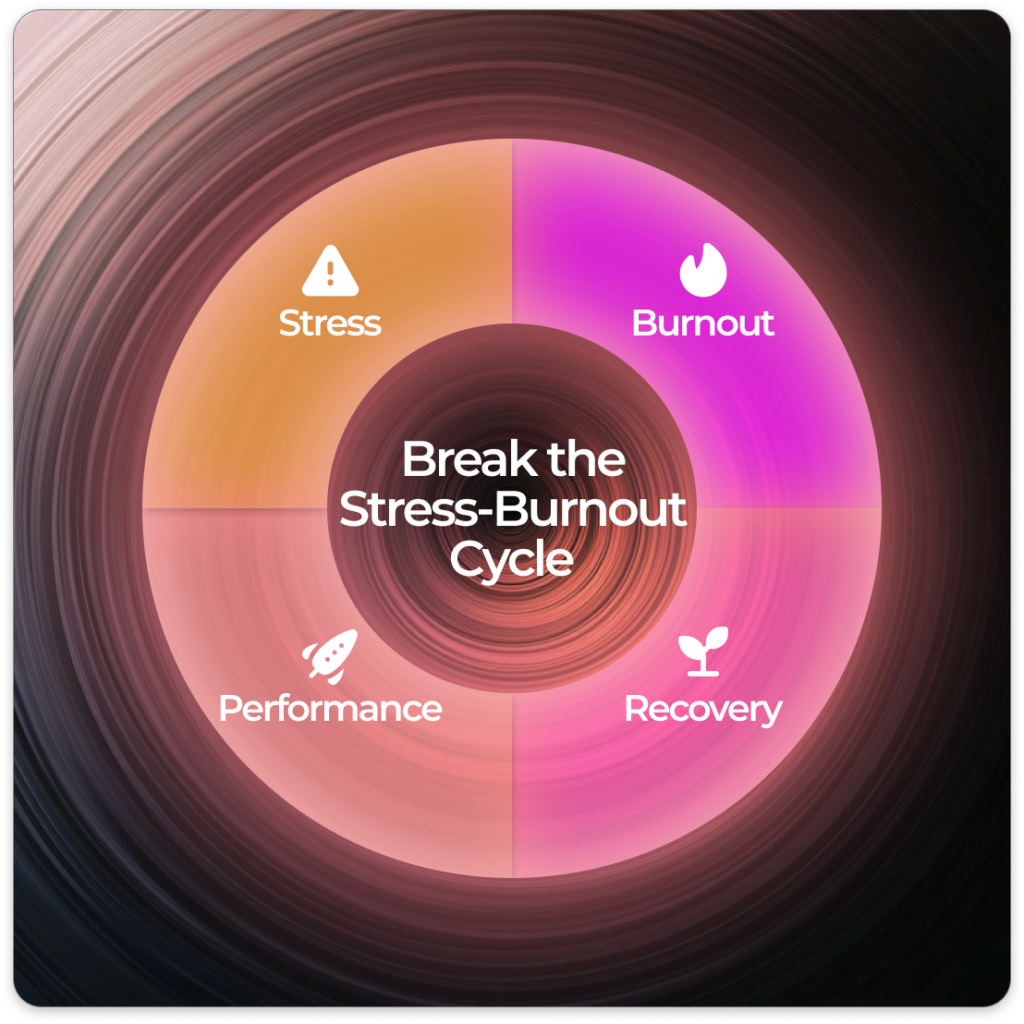

The Entrepreneur’s Challenge: Stress and Burnout

Entrepreneurs face unique pressures that often lead to stress and burnout. The demands of running a business can be relentless. This constant pressure takes a toll on mental and physical health.

Burnout occurs when stress becomes unmanageable. It results in exhaustion, detachment, and diminished performance. Entrepreneurs may struggle to maintain productivity and creativity during burnout.

Recognizing the signs of stress and burnout is crucial. Entrepreneurs need to monitor their stress levels. Proactively managing stress can prevent long-term damage.

Effective stress management starts with acknowledging the challenge. Developing coping strategies can protect an entrepreneur’s well-being. By addressing stress early, entrepreneurs can maintain their drive and passion for business.

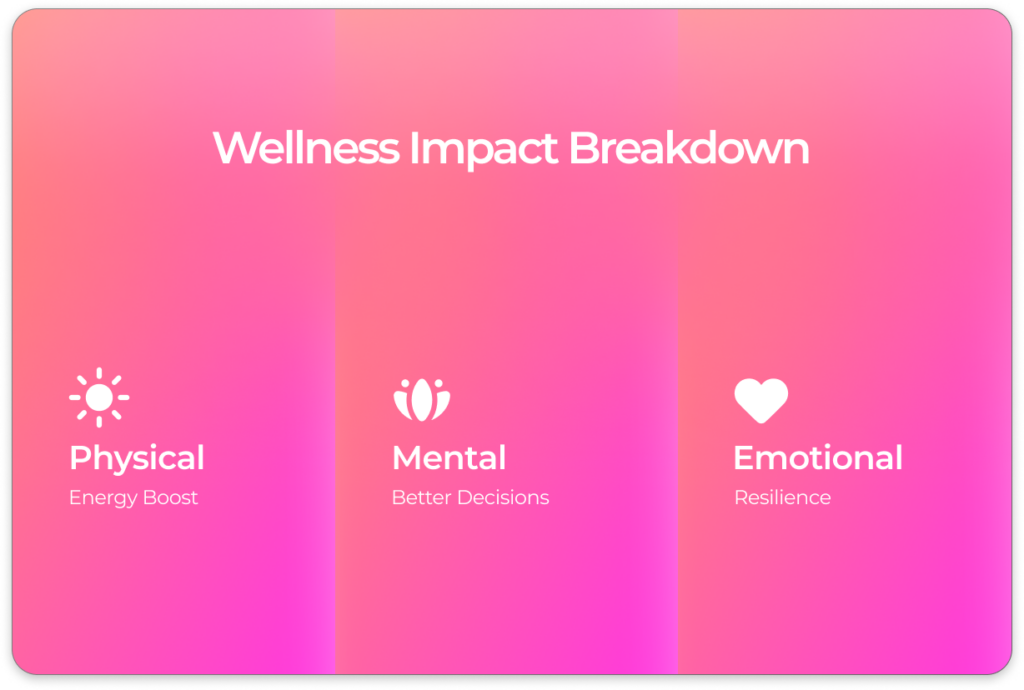

The Impact of Wellness on Decision-Making and Success

Wellness is a powerful catalyst for effective decision-making. Entrepreneurs with a balanced state of health often make clearer, more strategic choices. Mental clarity and calmness foster better business judgment.

Physical wellness contributes significantly to success. Entrepreneurs in good physical health experience increased energy and focus. This boost in vitality translates into sustained productivity.

Mental health is equally important in the entrepreneurial landscape. A sound mental state enhances emotional regulation. Entrepreneurs with strong mental wellness handle stressors with greater ease.

Incorporating wellness practices helps build a foundation for success. Prioritizing personal health leads to more sustainable business outcomes. Entrepreneurs find resilience in a holistic approach to wellness.

Strategies for Building Entrepreneurial Resilience

Building resilience is crucial for entrepreneurs facing constant challenges. It’s about developing the ability to bounce back stronger. Entrepreneurs can cultivate resilience through practical strategies and lifestyle changes.

Here are some effective strategies:

Set realistic goals: Achievable targets prevent overwhelm and instill confidence.

Maintain a positive outlook: Focus on potential rather than setbacks.

Foster a supportive network: Surround yourself with encouraging peers.

Embrace mindfulness: Practice staying present to reduce anxiety.

Adopting these strategies reinforces an entrepreneur’s ability to tackle adversity. A strategic approach involves both internal mindset shifts and external support systems. Building resilience isn’t a solitary endeavor—it requires community and consistency.

Setting Realistic Goals and Maintaining a Positive Outlook

Realistic goals are essential for sustained progress. Entrepreneurs should break down big ambitions into manageable steps. This approach makes daunting tasks feel achievable and reduces the risk of feeling overwhelmed.

A positive outlook plays a pivotal role in resilience. Focusing on solutions rather than problems boosts morale. Optimism doesn’t ignore challenges but reframes them as opportunities.

Entrepreneurs should celebrate small victories along the way. Recognizing progress, no matter how modest, fuels motivation. Positive reinforcement strengthens the belief in one’s capability to succeed.

Fostering a Supportive Network

A supportive network is vital for entrepreneurial resilience. Peers who understand the entrepreneurial journey provide invaluable encouragement. Having a circle that offers emotional and professional support enhances confidence.